Display panel shipments in the first quarter of 2020 31.4 million pieces, down 7.7% year-on-year; in terms of area the shipments were 5 million square meters, down 3.8% year-on-year, according to the latest report from market research agency Sigmaintell.

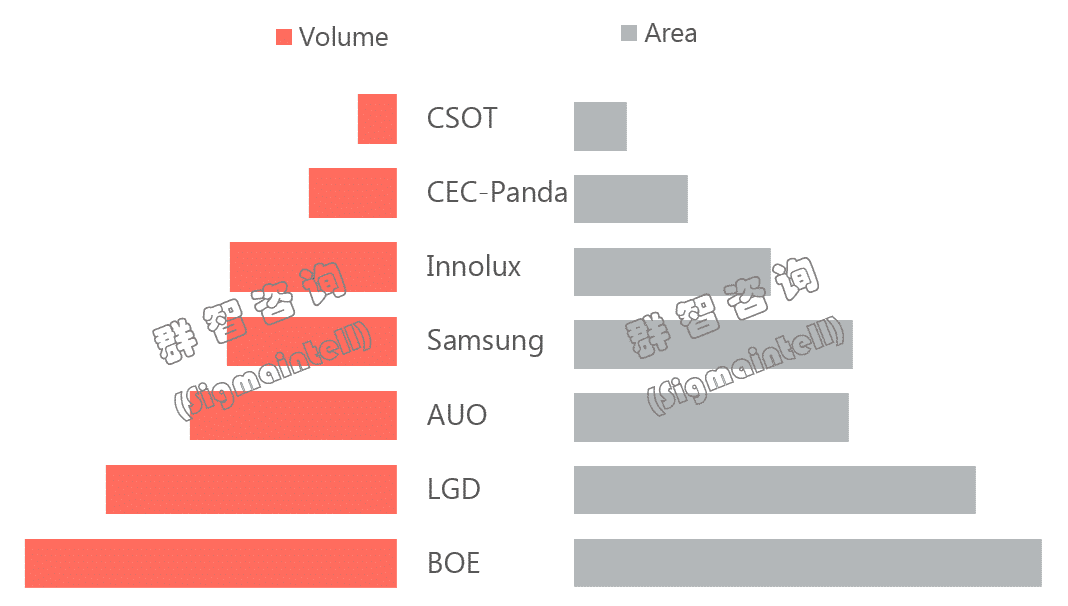

In terms of vendor rankings, BOE ranked first with 8.7 million pieces shipped, a 13% year-over-year increase.

In second place was LG Display (LGD), which shipped 6.9 million units, down 11 percent year-over-year.

AUO ranked third with 4.9 million tablets shipped, down 23% year-over-year.

Samsung, Innolux Corporation, CEC-Panda, and TCL CSOT are ranked in that order.

Sigmaintell believes that the reason for the BOE's negative growth is, on the one hand, that overall manufacturing is on the mainland and production resumes earlier, so it can be more flexible and proactive in dealing with the impact of the epidemic.

On the other hand is to focus on IPS technology and other better products, IPS technology shipments accounted for 75%, of which IPS e-competition also stable starting volume.

It is worth noting that for the first time, BOE overtook LGD in first place in terms of area shipped.

The decline in LGD and AU Optronics is due to the fact that the back-end production of the modules is located in mainland China, which was affected by the transportation and resumption of work policies during the outbreak.

In addition, for panel size trends, Sigmaintell noted that the average display panel size for the quarter was 24.0 inches, up 0.7 inches year-over-year and 0.2 inches in the ring.

In the second quarter, overseas market demand is strong, the domestic consumer market and Internet cafes gradually recover, the progress of large size will be maintained.