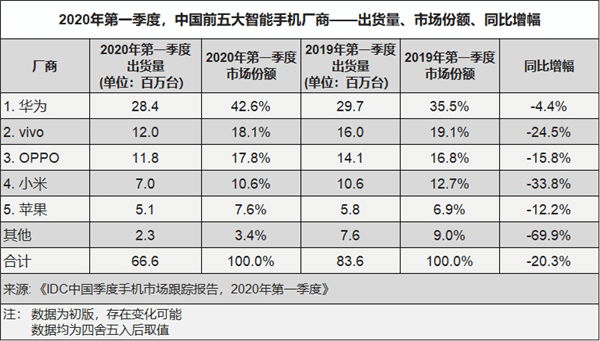

In the first quarter of 2020, the Chinese smartphone market shipped about 66.6 million units, down 20.3 percent year-on-year, according to a report released today by IDC.

According to IDC, the Chinese market declined significantly in the first quarter due to the novel coronavirus outbreak, but ultimately performed better than expected.

According to the report, Huawei ranks first with 42.6% market share, with VIVO (18.1%) and OPPO (17.8%) in second and third place. Xiaomi came in fourth with a 10.6% share and Apple fifth with a 7.6% share.

IDC says Huawei has achieved the best performance among China's top five manufacturers in a tough market environment.

During the epidemic, Huawei's offline stores of tablets, laptops, and other products have successfully helped Huawei generate greater pull in the limited offline traffic due to the climbing demand of users for online education and telecommuting.

The ecological advantages of Huawei's multi-device synergy have also driven mobile phone products to a certain extent.

In early March, the early price adjustment of flagship products, the glory of the brand's online promotion, also smoothly catered to the epidemic gradually improved after the release of terminal consumer demand, driving Huawei's overall market share continued to climb to a record high.

Relying on its rich online product line coverage, VIVO's online channel market performance was stable during the epidemic.

The iQOO and Z series of new products introduced to the market in February and March, in addition to continuing to focus on the online market, Vivo's 5G products quickly covered a wider range of price points and user groups.

OPPO continues to hold the third position, with a narrowing of the drop compared to the second half of 2019.

In the first quarter, the market performance of the Reno 3 series of products was stable, helping OPPO to consolidate the performance of the 5G market in the mid- to the high-end price point.

OPPO updated its high-end flagship Find X2 series in March, focusing more on the overall strength of the product and the long-term operational readiness of the high-end market and users than its more design-oriented predecessor.

Xiaomi was limited by the impact of the epidemic on supply chain capacity, as well as low inventory levels, which generated a certain amount of shortages in the first half of the first quarter, affecting its overall performance.

In the second half of the first quarter, Xiaomi and Redmi flagship products have a more obvious distinction in product experience and user positioning, jointly covering the price segment of more than 3,000 yuan to impact the high-end market.

In addition to product configuration strength, Xiaomi's future development in the high-end market will require continuous attention to high-end users and channels, long-term claims, and operations.

Apple has been affected by the outbreak, and the related supply chain has been hit more than other Android manufacturers in China.

On the retail end, Apple's direct store channel has a larger share of the market compared to other Android manufacturers in China, and the store closures during the epidemic have further impacted Apple's market performance.

In the first quarter, Apple shipped about 5.1 million units in China.