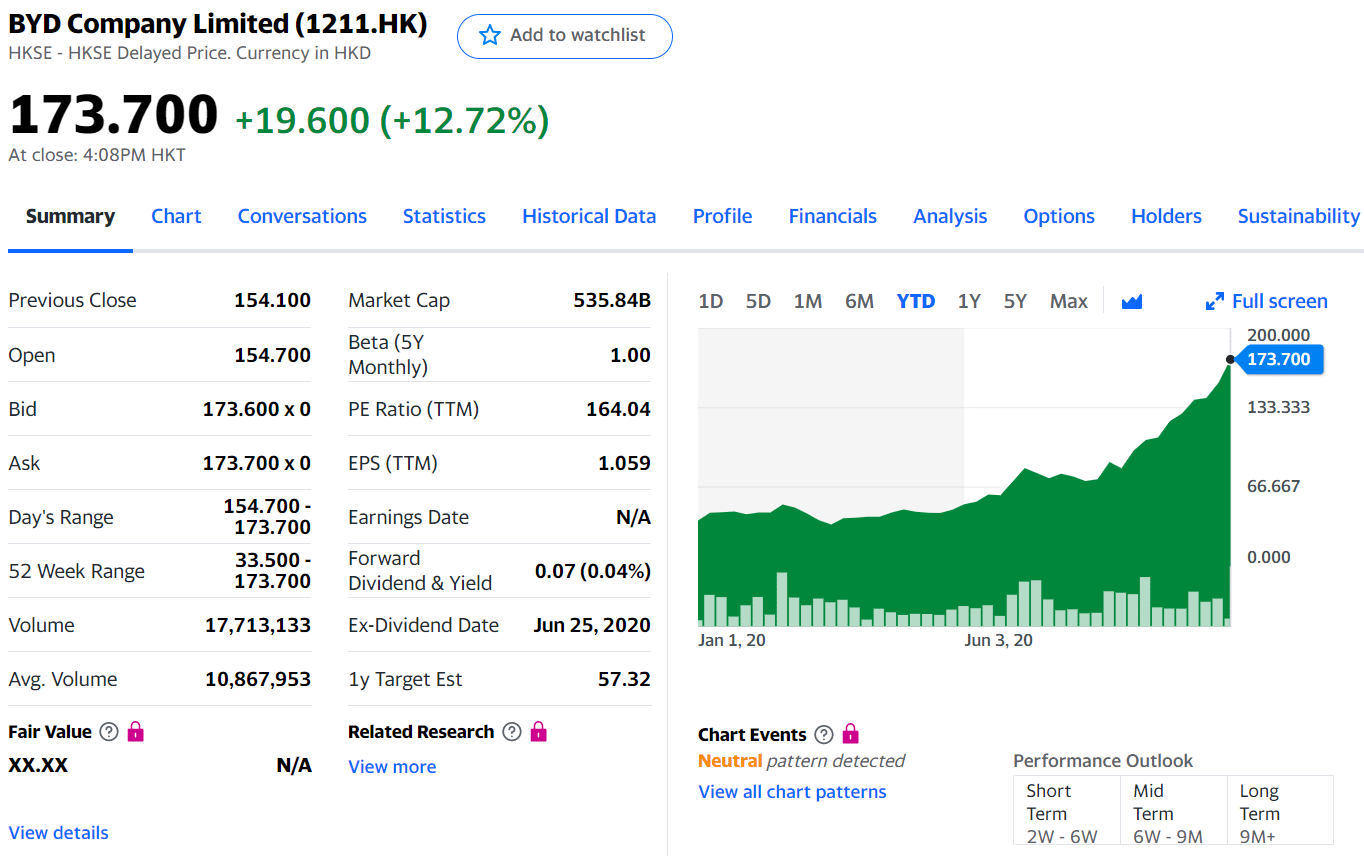

CLSA reiterated its "buy" recommendation on Hong Kong-traded BYD Company Limited (01211.HK) in a recent report, raising the target price by 45% from HK$131 to HK$190, which is 9.38% higher than the company's closing price on Monday.

The target price is equivalent to 3.9 times next year's enterprise value to sales forecast, enterprise value to 27 times EBITDA.

The automotive market continues to recover thanks to a favorable EV and battery product cycle, and BYD's fiscal 2020 third-quarter results exceeded market expectations due to strong electric vehicle (EV) sales.

CLSA said BYD is attracting more external customers and has become an EV solution provider by providing battery and semiconductor business to external companies.

BYD's market cap exceeds that of NIO and Li Auto combined, how did it do it?

So far, the company has received battery orders from BAIC and Ford, while orders from other global OEMs such as Toyota and Hino are likely to materialize in the next few years.

CLSA forecasts that BYD's external battery sales will account for half of its total battery shipments by 2025, up from just 2 percent last year.

CLSA said it decided to raise its forecast for BYD's net profit for 2020-2022 by 17.6%, 17.8% and 9.4% to CNY4.128 billion, CNY4.505 billion and CNY4.669 billion, based on BYD's performance and believes its growth potential warrants a valuation premium.

CLSA said the company's catalysts include strong sales of its flagship electric vehicles, battery supply contracts with external automakers, and potential spin-offs of its semiconductor and battery businesses.